The collapse of the bubble has created a situation where, at least as far as real estate is concerned, there is nothing left to steal.“Equity stripping is largely a thing of the past because there’s no equity to strip,” said [DOJ official] Perez.H/T Daily Caller

“Equity stripping” is a scam where con-artists persuade confused or ill-prepared people to sign home-loan contracts that transfer the property rights. Victims — often old or ill-educated — are left without their homes, but with much new debt.

Instead of equity stripping, the con artists are moving to new areas, Perez said.

Showing posts with label real estate bubble. Show all posts

Showing posts with label real estate bubble. Show all posts

Sunday, May 6, 2012

"Equity Stripping" scams on the decline

Real estate scams are apparently on the decline as the real estate bubble continues its collapse:

Thursday, October 20, 2011

Homeownership decline in 2010

The AP and the Census Bureau report that homeownership saw continued nationwide declines in 2010:

The American dream of homeownership has felt its biggest drop since the Great Depression, according to new 2010 census figures released Thursday.

The analysis by the Census Bureau found the homeownership rate fell to 65.1 percent last year. While that level remains the second highest decennial rate, analysts say the U.S. may never return to its mid-decade housing boom peak in which nearly 70 percent of occupied households were owned by their residents.

Monday, May 23, 2011

Glut of foreclosed homes may deepen real estate downturn.

A recent article in the New York Times estimates that lenders own more than 872,000 foreclosed homes at this time:

For each home a lender sells, they foreclose on many more:

The problem is apparently widespread and will contribute to continuing stagnation for several more years.

All told, they own more than 872,000 homes as a result of the groundswell in foreclosures, almost twice as many as when the financial crisis began in 2007, according to RealtyTrac, a real estate data provider. In addition, they are in the process of foreclosing on an additional one million homes and are poised to take possession of several million more in the years ahead.

For each home a lender sells, they foreclose on many more:

In Atlanta, lenders are repossessing eight homes for each distressed home they sell, according to March data from RealtyTrac. In Minneapolis, they are bringing in at least six foreclosed homes for each they sell, and in once-hot markets like Chicago and Miami, the ratio still hovers close to two to one.

Before the housing implosion, the inflow and outflow figures were typically one-to-one.

The problem is apparently widespread and will contribute to continuing stagnation for several more years.

Wednesday, January 12, 2011

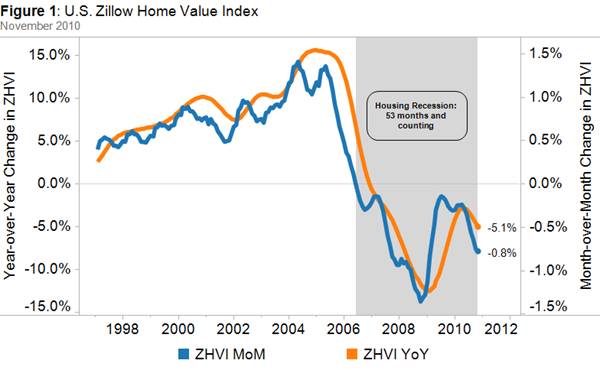

Housing market entering depression status nationwide

CNBC reported yesterday that the housing market nationwide is now officially in a "depression":

Zillow includes the following graph:

Zillow housing graph

Zillow housing graph

Each year in gray shows a decline. The uptick following 2008 is merely a decline in the rate of decrease, not an actual increase in values or prices.

While most commentators think that the housing market will improve only when employment numbers improve, the real cure for this depression would be for the government to allow prices to fall. At some point, prices would finally reach the point where they should be - where real estate is affordable to consumers without the need for a credit bubble to spur buying. The government only delays this process by propping up prices with stimulus money, targeted tax credits, etc.

Home values have fallen 26 percent since their peak in June 2006, worse than the 25.9-percent decline seen during the Depression years between 1928 and 1933, Zillow reported.

November marked the 53rd consecutive month (4 ½ years) that home values have fallen.

What’s worse, it’s not over yet: Home values are expected to continue to slide as inventories pile up, and likely won't recover until the job market improves.

Zillow includes the following graph:

Zillow housing graph

Zillow housing graphEach year in gray shows a decline. The uptick following 2008 is merely a decline in the rate of decrease, not an actual increase in values or prices.

While most commentators think that the housing market will improve only when employment numbers improve, the real cure for this depression would be for the government to allow prices to fall. At some point, prices would finally reach the point where they should be - where real estate is affordable to consumers without the need for a credit bubble to spur buying. The government only delays this process by propping up prices with stimulus money, targeted tax credits, etc.

Monday, June 28, 2010

"Downfall;" Hitler explains the real estate collapse

By now, everyone has a "Downfall" movie parody relating to the issue of the moment. (I even saw a "Downfall" parody about the vuvuzelas that have annoyed so many soccer viewers recently.)

So I would be remiss if I did not include a copy of a "Downfall" parody that explains the real estate collapse.

So I would be remiss if I did not include a copy of a "Downfall" parody that explains the real estate collapse.

Friday, June 11, 2010

Deflation and gasoline prices.

This article indicates that the U.S. money supply has declined rapidly in recent months, despite runaway government spending.

How this could happen would be the subject of a full length textbook. Suffice it to say that the money supply is composed of many elements, including bank loans. When credit is tight, the money supply gets smaller, regardless of government spending.

A major indicator of the direction of inflation is the price of gasoline. The price of gasoline fell during and immediately before Memorial Day weekend. The price has not moved back up since then. It is unusual for gasoline prices to fall before and during a summer holiday. It is unusual for any prices to fall during a period of runaway government spending.

It is possible that the credit bubble that begin its collapse around 2007 is still collapsing - that the government stimulus bill (and related spending) is merely delaying the collapse. If that is true, the deflation we are experiencing is, ultimately, a good thing. The economy will not turn around until prices get to where they are going, even though the ride down will be painful.

If this scenario is allowed to play out, it would mean lower prices for real estate (accompanied by pain, foreclosures, bankruptcy, etc.), but, ultimately, an increase in sales at the new lower price levels.

How this could happen would be the subject of a full length textbook. Suffice it to say that the money supply is composed of many elements, including bank loans. When credit is tight, the money supply gets smaller, regardless of government spending.

A major indicator of the direction of inflation is the price of gasoline. The price of gasoline fell during and immediately before Memorial Day weekend. The price has not moved back up since then. It is unusual for gasoline prices to fall before and during a summer holiday. It is unusual for any prices to fall during a period of runaway government spending.

It is possible that the credit bubble that begin its collapse around 2007 is still collapsing - that the government stimulus bill (and related spending) is merely delaying the collapse. If that is true, the deflation we are experiencing is, ultimately, a good thing. The economy will not turn around until prices get to where they are going, even though the ride down will be painful.

If this scenario is allowed to play out, it would mean lower prices for real estate (accompanied by pain, foreclosures, bankruptcy, etc.), but, ultimately, an increase in sales at the new lower price levels.

Monday, November 30, 2009

Suburban development trends

The USA Today published an item this month regarding suburgan development trends throughout the United States. The paper noted the end of four decades of suburban growth throughout the nation:

What does this mean for Central Pennsylvania? We have not suffered the same consequences as the Sun Belt cities during the recent economic downturn, thus indicating that real estate is not the real "economic engine" for Central Pennsylvania. Instead, government employment has been the main economic engine in the Harrisburg area and continues to prop up the real estate business locally (with help from stimulus money and homebuyers credits).

Does this mean that the real estate bubble is safe in Central Pennsylvania forever? Will real estate prices forever rise? Don't count on it.

"Places that have done the worst are places where basically real estate was the economic engine," says Ed McMahon, senior research fellow at the Urban Land Institute, a non-profit group that promotes sustainable development.emphasis added

What does this mean for Central Pennsylvania? We have not suffered the same consequences as the Sun Belt cities during the recent economic downturn, thus indicating that real estate is not the real "economic engine" for Central Pennsylvania. Instead, government employment has been the main economic engine in the Harrisburg area and continues to prop up the real estate business locally (with help from stimulus money and homebuyers credits).

Does this mean that the real estate bubble is safe in Central Pennsylvania forever? Will real estate prices forever rise? Don't count on it.

Saturday, October 31, 2009

Congress ready to extend the real estate bubble; Homebuyers' tax credit

Congress apparently intends to extend the tax credit now in place for first time home buyers:

The credit would be extended through April and a new credit of $6,500.00 would be added for existing homeowners to buy new homes.

[The following analysis was written mainly with the Central Pennsylvania real estate market in mind.]

While this news may be welcomed by the real estate industry, it contains hidden consequences. The real estate bubble burst for a reason. Houses were overpriced, lenders were overextended and the economy could not sustain the false prosperity. We cannot get rich as a nation by trading the same real estate with each other at constantly increasing prices. The government can reinflate the bubble only for so long.

.jpg)

The only real cure is to allow prices to fall so that the real estate inventory can clear. There are deals to be made and there is money to be invested, but that will not happen if the government keeps propping up prices and turning what should be a buyers' market into a sellers' market. I have personally witnessed sellers that stuck to their unrealistic bubble inspired asking prices because the tax credit program was feeding new buyers to them. I have seen first time buyers feel pressured into paying too much for a home (or into buying a home with defects) because of the approaching expiration of the tax credit program.

Buyers who see the immediate cash benefit of the tax credit often fail to realize that this tax credit is reflected in the price of the house.

With foreclosures at an all time high, this is supposed to be a buyers' market. We are bombarded with advertisements explaining how we can obtain good deals now at rock bottom prices. But it appears, instead, that we are seeing the worst of both worlds. Foreclosures continue at a record pace while prices remain high and unrealistic.

The real effect of the home buyer tax credit program will be to bail out sellers that paid too much for their homes during the bubble, while creating a whole new group of victims (the buyers) that will need to be rescued when the new bubble collapses.

Senate leaders have reached a tentative deal to extend the first-time homebuyers' tax credit that was originally passed earlier this year as part of the stimulus bill, Republican and Democratic sources told CNN on Wednesday.

The credit would be extended through April and a new credit of $6,500.00 would be added for existing homeowners to buy new homes.

[The following analysis was written mainly with the Central Pennsylvania real estate market in mind.]

While this news may be welcomed by the real estate industry, it contains hidden consequences. The real estate bubble burst for a reason. Houses were overpriced, lenders were overextended and the economy could not sustain the false prosperity. We cannot get rich as a nation by trading the same real estate with each other at constantly increasing prices. The government can reinflate the bubble only for so long.

.jpg)

The only real cure is to allow prices to fall so that the real estate inventory can clear. There are deals to be made and there is money to be invested, but that will not happen if the government keeps propping up prices and turning what should be a buyers' market into a sellers' market. I have personally witnessed sellers that stuck to their unrealistic bubble inspired asking prices because the tax credit program was feeding new buyers to them. I have seen first time buyers feel pressured into paying too much for a home (or into buying a home with defects) because of the approaching expiration of the tax credit program.

Buyers who see the immediate cash benefit of the tax credit often fail to realize that this tax credit is reflected in the price of the house.

With foreclosures at an all time high, this is supposed to be a buyers' market. We are bombarded with advertisements explaining how we can obtain good deals now at rock bottom prices. But it appears, instead, that we are seeing the worst of both worlds. Foreclosures continue at a record pace while prices remain high and unrealistic.

The real effect of the home buyer tax credit program will be to bail out sellers that paid too much for their homes during the bubble, while creating a whole new group of victims (the buyers) that will need to be rescued when the new bubble collapses.

Monday, October 26, 2009

More casualties of the real estate bubble?; Stuyvesant Town and Peter Cooper Village; Manhattan disaster to cost Florida and California pensioners?

From New York City (via AP) comes the story of the largest ever U.S. real estate deal heading toward bankruptcy, foreclosure or both:

Click here for more background on the original purchase. In addition to the bubble collapse that has devastated so much of the real estate market, this particular deal has been hampered by lawsuits from tenants resisting the new owners' conversion to higher priced units:

The AP article speculates on foreclosure possibilities. The bottom line is that a court's proclivity to limit rent may partially contribute to history's most costly foreclosure. If you are thinking "so what?" consider the following:

The real estate bubble will affect everyone, even those who did not know that they were participating. The consequences in this case are being aggravated by rent limits being imposed by the courts.

Stuyvesant Town and Peter Cooper Village (New York Times photo)

Stuyvesant Town and Peter Cooper Village (New York Times photo)

It was the most expensive real estate deal in U.S. history. Now it's poised to become one of the biggest flops.

At the height of the real estate bubble in 2006, an investment group led by New York City real estate firm Tishman Speyer Properties and BlackRock Realty Advisors paid $5.4 billion for a pair of gigantic Manhattan apartment complexes known as Stuyvesant Town and Peter Cooper Village.

Click here for more background on the original purchase. In addition to the bubble collapse that has devastated so much of the real estate market, this particular deal has been hampered by lawsuits from tenants resisting the new owners' conversion to higher priced units:

Tenants fought back, conversions happened much slower than expected and a state court ruled Thursday that about $200 million in the company's new rent increases were improper.

The AP article speculates on foreclosure possibilities. The bottom line is that a court's proclivity to limit rent may partially contribute to history's most costly foreclosure. If you are thinking "so what?" consider the following:

Some of the biggest equity investors in the deal are public pension funds that manage retirement system benefits for millions of government employees.

Florida's State Board of Administration had put $250 million into the project. It has already written off the entire investment as a loss.

California's two largest government pension funds, the California Public Employees' Retirement System and the California State Teachers Retirement System, invested a combined $600 million. CalSTRS has also already written off its $100 million stake.

The real estate bubble will affect everyone, even those who did not know that they were participating. The consequences in this case are being aggravated by rent limits being imposed by the courts.

Stuyvesant Town and Peter Cooper Village (New York Times photo)

Stuyvesant Town and Peter Cooper Village (New York Times photo)

Thursday, October 15, 2009

More foreclosure bad news; CNN

CNN reports more foreclosure bad news today:

CNN cites nationwide data and specific data for Nevada and Vermont. My own observations (and those of associated professionals) is that central Pennsylvania foreclosures appear to have been generally steady during 2009.

The bad news relates to foreclosures that are still to come. Banks have been slower to initiate foreclosures (both nationally and locally) than in prior years:

Lenders are also slow to dump delinquent properties back on the market for fear of causing a free fall in real estate prices. Foreclosures tend to depress real estate prices in general, not merely the prices of foreclosed properties. If real estate prices spiral downward, existing homeowners will not be able to sell or refinance their homes due to lack of equity. This problem will result in more foreclosures and a worsening real estate downward spiral.

We are witnessing the bursting of a very deep bubble.

Despite concerted government-led and lender-supported efforts to prevent foreclosures, the number of filings hit a record high in the third quarter, according to a report issued Thursday.

"They were the worst three months of all time," said Rick Sharga, spokesman for RealtyTrac, an online marketer of foreclosed homes.

CNN cites nationwide data and specific data for Nevada and Vermont. My own observations (and those of associated professionals) is that central Pennsylvania foreclosures appear to have been generally steady during 2009.

The bad news relates to foreclosures that are still to come. Banks have been slower to initiate foreclosures (both nationally and locally) than in prior years:

[T]he RealtyTrac statistics may understate the depth of the foreclosure mess because lender and government actions have delayed many filings. As a result, some delinquencies have not been counted on the foreclosure tallies. That means the crisis may not end quickly.

Lenders are also slow to dump delinquent properties back on the market for fear of causing a free fall in real estate prices. Foreclosures tend to depress real estate prices in general, not merely the prices of foreclosed properties. If real estate prices spiral downward, existing homeowners will not be able to sell or refinance their homes due to lack of equity. This problem will result in more foreclosures and a worsening real estate downward spiral.

We are witnessing the bursting of a very deep bubble.

Thursday, October 8, 2009

Home equity, savings and the current economic crisis.

A recent quote from David Goldman ("Spengler") helps put the role of home equity in context in today's economic crisis:

Remember, equity in an inflated asset does not take the place of actual savings.

Americans have saved almost nothing during the past 10 years, relying instead on home equity that now has vaporized. The proportion of Americans over 60 will jump to 25% from 19% during the next 10 years, an unprecedented shift. Americans must save to compensate for past profligacy, from a lower starting point after the destruction of so much wealth, and with lower prospective returns.

Remember, equity in an inflated asset does not take the place of actual savings.

Saturday, September 26, 2009

Adjustable rate mortgage defaults and lending industry consolidation.

Reuters warned last week of the next round in the ongoing financial crisis:

The impact of this round of foreclosures could be severe:

The loss for lenders on each "jumbo" mortgage foreclosure would be greater than the losses on smaller loans.

All of this bad news makes the following item even more interesting:

While this second item refers to new mortgages instead of the existing ARM mortgages of the first article, it should cause great concern that lenders are about to take another round of bad hits just as the mortgage industry seems to be consolidating into only three major institutions.

The articles cited above were speaking of national trends. But someday, this crisis has to reach the point where even the supposedly stable Central Pennsylvania market will feel the effects of the credit crunch more sharply than it has thus far.

The federal government and states are girding themselves for the next foreclosure crisis in the country's housing downturn: payment option adjustable rate mortgages that are beginning to reset.

"Payment option ARMs are about to explode," Iowa Attorney General Tom Miller said after a Thursday meeting with members of President Barack Obama's administration to discuss ways to combat mortgage scams.

The impact of this round of foreclosures could be severe:

The mortgages tend to be "jumbo," or for significantly large amounts, Goddard said, making it even harder for borrowers to sidestep foreclosure. He said he expected to see an increase in scams as distressed homeowners become more desperate to refinance big debts.

The loss for lenders on each "jumbo" mortgage foreclosure would be greater than the losses on smaller loans.

All of this bad news makes the following item even more interesting:

Peter Eavis, writing in the Wall Street Journal on Friday [September 18, 2009], noted: "More than half of US residential mortgages are being made by just three large banks. It is a stunning change, but is it good for the housing market, and to what extent will it boost profits over the long term for this elite trio: Wells Fargo, Bank of America, and JP Morgan Chase? Right now, housing remains on government life support. Treasury-backed entities are guaranteeing about 85% of new mortgages, while the Fed buys 80% of the securities into which these taxpayer-backed mortgages are packaged."

While this second item refers to new mortgages instead of the existing ARM mortgages of the first article, it should cause great concern that lenders are about to take another round of bad hits just as the mortgage industry seems to be consolidating into only three major institutions.

The articles cited above were speaking of national trends. But someday, this crisis has to reach the point where even the supposedly stable Central Pennsylvania market will feel the effects of the credit crunch more sharply than it has thus far.

Subscribe to:

Posts (Atom)